Millennials have a reputation for financial irresponsibility. From the amount of avocado toast they allegedly order to their disinterest in investing in a home and renting instead, people really enjoy giving this generational group a hard time. They’ve even gone so far as to say millennials have killed banks, home-ownership, and casual-dining restaurant chains.

Do millennials really deserve to be the subject of these harsh assumptions? And how true are all of the claims people make about millennials’ frivolous spending habits and lack of savings plans? In order to find out, we surveyed 600 millennials between the ages of 23 and 38 on both their spending and saving habits. Read on to learn more about what we uncovered.

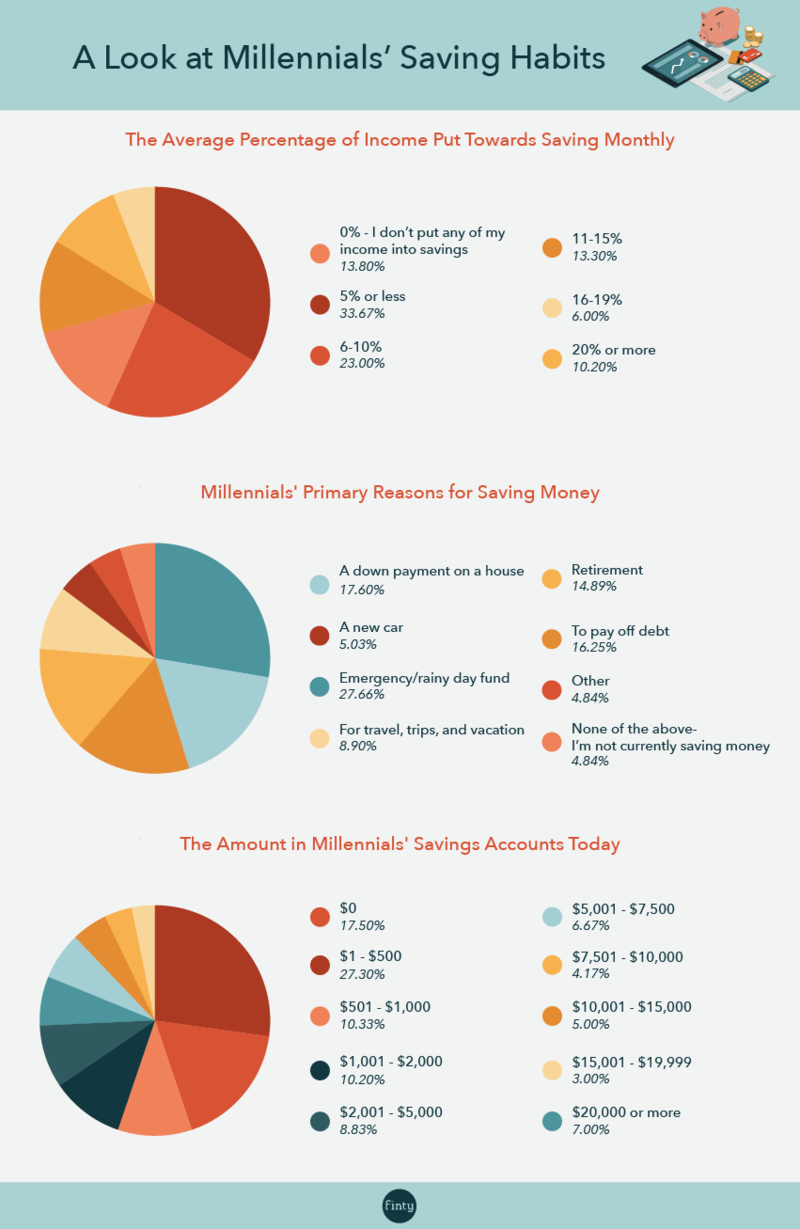

We first dug into millennials’ spending habits, starting with whether they have a regular savings strategy in place. We found that about 86% of millennials were setting aside at least some amount of money each month. About 1 in 3 millennials save 5 percent or less of their monthly income and about 1 in 4 save somewhere between 6 to 10 percent.

For the millennials that are saving money, the most common purpose for saving is to build an emergency or rainy-day fund. Saving for a down payment on a house and repaying debts are the second and third most common reasons. Only 12.8% of millennials cite retirement as their primary reason for saving. Of the millennials saving for a down payment on a home, most of them think they’ll be in the right financial situation to buy by age 31 - 33.

And how is that saving adding up? For the 17.5% of millennials with empty savings accounts, not so well. That’s not the case for all though, the other 82.5% have at least some money in savings, even if it’s $1,000 or less for nearly half of respondents.

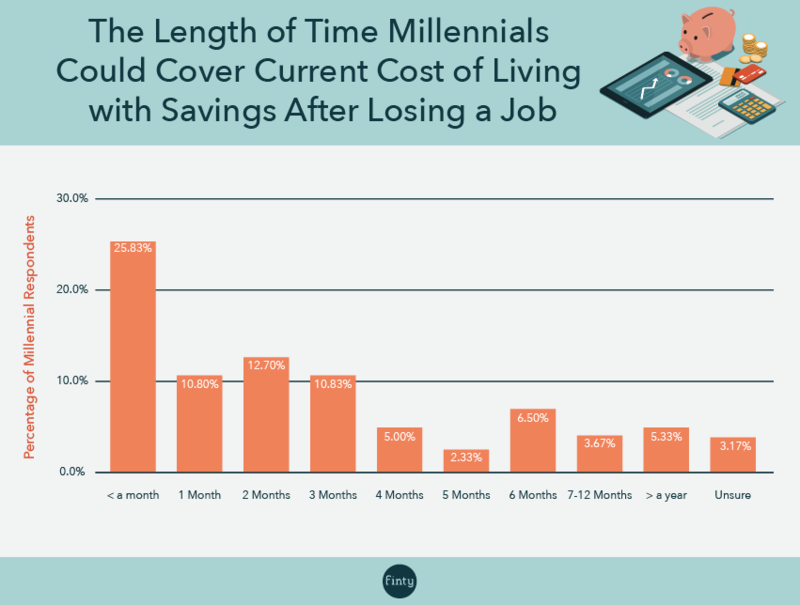

Even if many millennials do have spending strategies and are building their savings accounts, how prepared would they be if an emergency arose? It’s recommended that people have enough in savings to cover 6 months of living expenses to account for possible occurrences such as a job loss or unexpected illness. As shown above, about 1 in 4 millennials couldn't cover 1 month of living expenses with their savings if a situation of this kind arose. Only 15.5% of millennials’ savings accounts meet the 6-month recommendation.

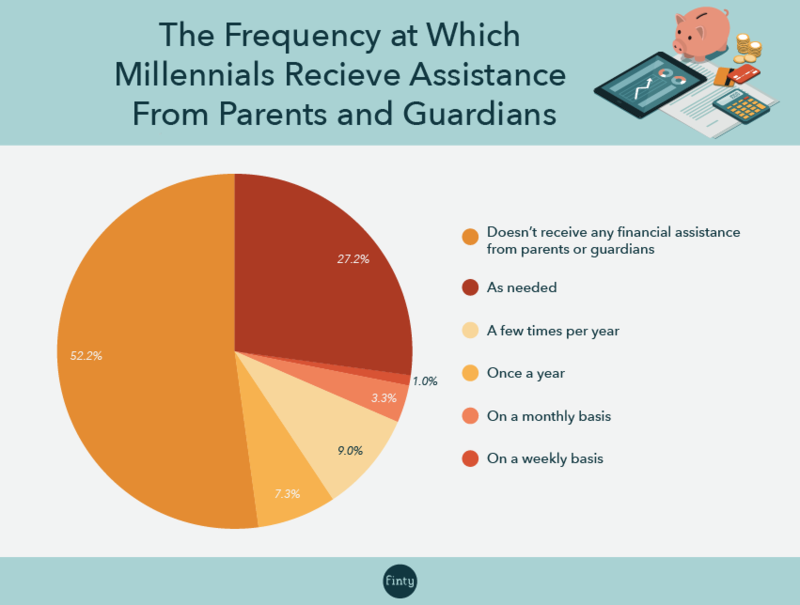

Given the lack of savings many millennials have built up, they likely need to turn to other avenues for money as needed. A parent or guardian would make sense as a common source of assistance. We asked millennials how often they receive financial assistance from their parents or guardians and found that nearly half receive some sort of assistance, however small. A very small percentage of millennials are receiving monthly or weekly financial support, but for most, it is a few times per year occurrence.

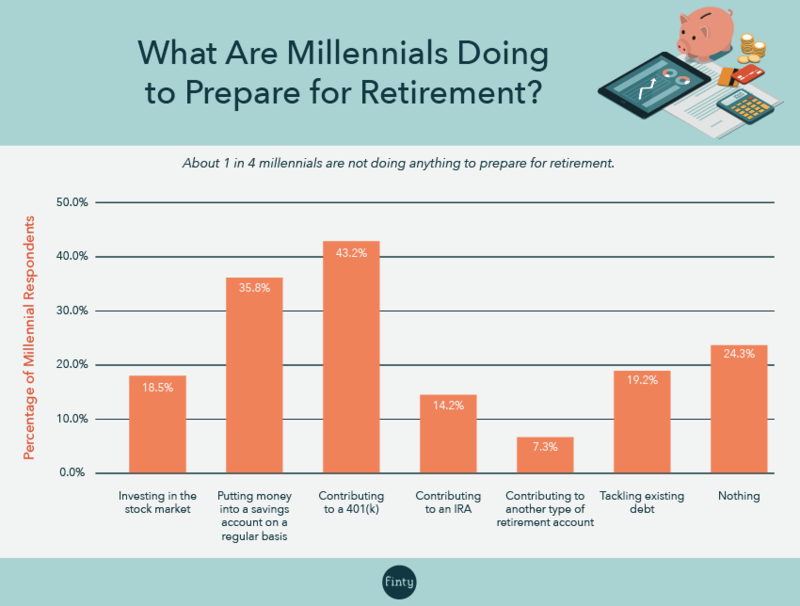

The last savings-related topic we explored was the steps that millennials are taking to prepare for retirement. While most millennials are still many years away from retiring, it’s ideal to begin thinking about retirement as early as possible. Surprisingly, about 1 in 4 millennials are currently not doing anything to prepare for retirement. Of the 3 in 4 that are taking steps to save for retirement, the most common actions they are taking are contributing to a 401(k) (43.2%), putting money in a savings account on a regular basis (35.8%), and tackling their existing debt (19.2%).

After gaining a thorough understanding of millennials’ savings habits, we switched gears to explore their spending habits. We asked respondents questions about their regular spending and expenses for things like food delivery, subscription services, and travel. Our findings do not align with the frivolous manner in which millennials are often portrayed.

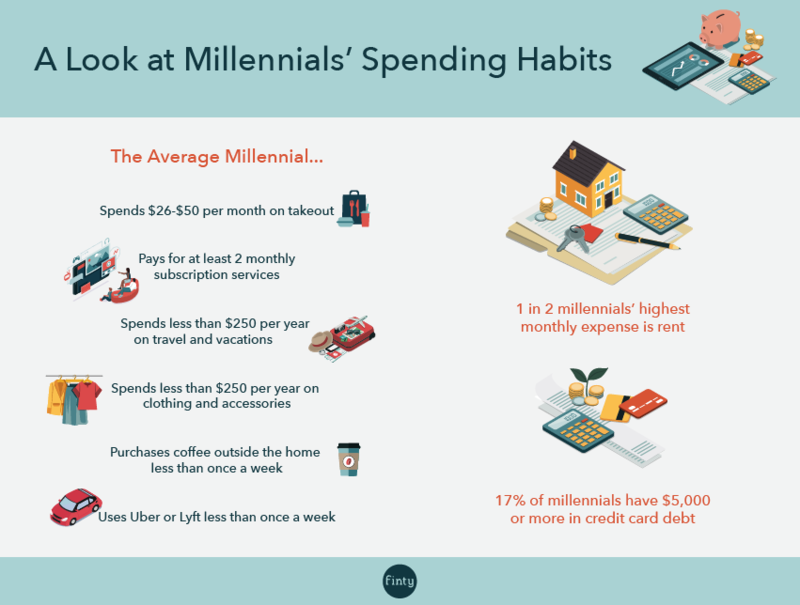

From a monthly perspective, rent is the highest monthly expense for about 1 in 2 millennials, though 15.8% of millennials surveyed live with parents or family members and are not currently paying rent. Beyond rent, millennials’ monthly spending includes 2 monthly subscription services and up to $50 on food delivery.

Millennials purchase coffee outside of home only about once a week and use rideshare apps like Uber, Lyft, or Grab at the same frequency. On an annual basis, the majority of millennials polled spend $250 or less on both travel and clothing and accessories.

Of course, millennials are extremely savvy in how they spend their money. Travel hacking, a.k.a. earning rewards with a credit card that can be redeemed for aspirational travel is widely practiced, as is getting cashback on credit card spend. More recently there has been a change in the perceived risk of debt brought about by the global financial crisis of 2017/18 and radical changes in the labour market. Millennials increasingly want to live a simpler and often footloose or nomadic life where they have no debt, with many following the principals of F.I.R.E. (Financial Independence Retire Early) in order to do so. A side effect of this has been the rising popularity of buy now pay later services and using personal loans to consolidate debts and get debt-free.

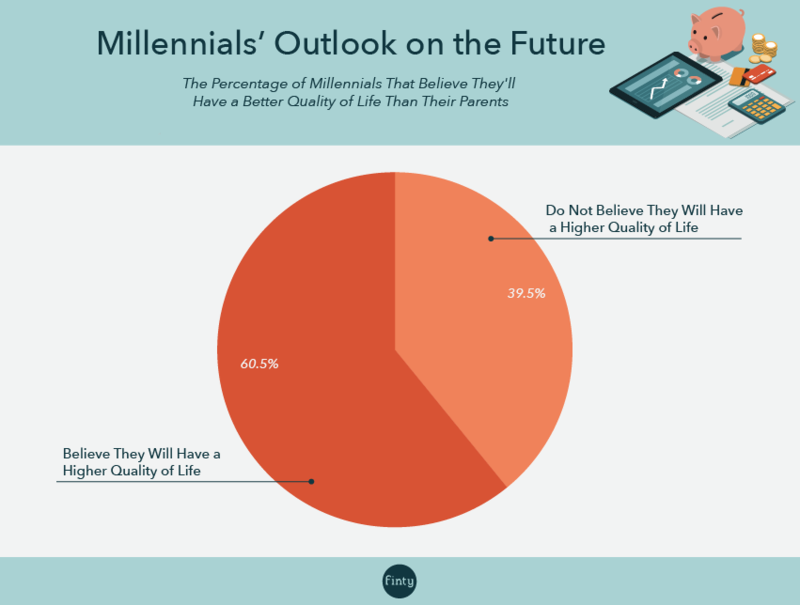

Finally, what does all of this mean for millennials’ financial futures? About 2 in 5 millennials do not believe they will have a higher quality of life than the parents. Luckily, there’s still plenty of time to turn that sentiment around by setting up healthy saving habits and strategies to ensure their future is as bright as it should be.

In conclusion, while millennials' spending habits didn’t line up with the ways in which they’re often portrayed, there is an opportunity for smarter saving strategies to help them prepare for the future.